When you have debt, it can be easy to let paying off debt become your primary focus. Your only goal is to pay it off as quickly as possible.

But actually, if you want to set yourself up for long-term success and pay down debt effectively and as quickly as possible, there are some things that you need to do BEFORE you start to pay down debt.

Today, I’m going to tell you about 5 things you need to do before you pay down debt.

Things to do BEFORE paying down debt

1) Don’t spend more than you bring in

Before you can take any steps toward paying off debt, you need to make sure that you have more money coming into your bank account than you have going out.

If your money isn’t growing every month, you have two options:

- Lower your expenses

Take a good, hard look at your expenses and think about how you can cut them down.

There may be obvious expenses you can cut out, like streaming services you don’t need or a gym membership you don’t use.

But it might be worth seeing if you can cut down on necessities. For example, could you move in with your parents or to an apartment building with cheaper rent?

Moving forward, develop mindful shopping habits. Before you make a purchase, ask yourself if it aligns with your values, if you need it, and how it will contribute to your wellbeing.

- Increase your income

If you can’t significantly cut down on expenses, then consider ways to increase your income, such as taking on a part-time job, freelancing, or selling unused items. Applying extra income directly towards your debt can help you pay it off faster.

Or, you can launch a side hustle, potentially starting something that's personally fulfilling AND earns you money!

2) Build an emergency fund

Before focusing on paying down debt, it's wise to have some savings set aside for emergencies. That way, if your dog finds and gobbles down your hidden chocolate stash or your washer breaks, it doesn’t interfere with your ability to pay your bills and make your debt payments because you have the money to deal with those things.

Aim to have at least $1000 saved up before you start paying down debt.

Everything you need to know about emergency funds!

.png)

3) Negotiate your interest rates

Contact your creditors to see if you can negotiate lower interest rates on your debts. Sometimes, they may be willing to work with you, especially if you have a good payment history.

We have an article on how to negotiate with credit card companies, but here are a few quick tips:

- Understand your financial situation, including how much you owe, your income, expenses, and any assets you have.

- Communicate early and respectfully

- Be prepared with what you can reasonably pay and what you want to ask for

4) Consider debt consolidation

If you're struggling to pay off a large amount of debt or a large number of debts, then debt consolidation may make the situation more manageable and less complex.

Learn more about debt consolidation!

Debt consolidation rolls multiple debts and typically high interest rate debt, such as credit card debt, into one single payment, making it easier to manage your debt and pay it off faster.

Debt consolidation might be a good idea for you if you can qualify for an interest rate that is lower than what you are currently paying on your current debts. That will help you reduce the total amount that you pay to get out of debt overall.

So you may want to consider debt consolidation if:

- Your monthly debt payments, including your rent or mortgage, are below 50% of your monthly income before taxes.

- Your credit is good enough to qualify for a 0% credit card or a low interest personal or debt consolidation loan. And typically this means having a credit score of about 690 or higher.

- Your monthly cash flow consistently covers the payments towards your debt

- You can choose a consolidation loan that you would be able to pay off within five years. Those are some good things to look for to see if debt consolidation is a good option for you.

5) Develop a debt pay down plan

The final step is to develop a plan for paying down your debt.

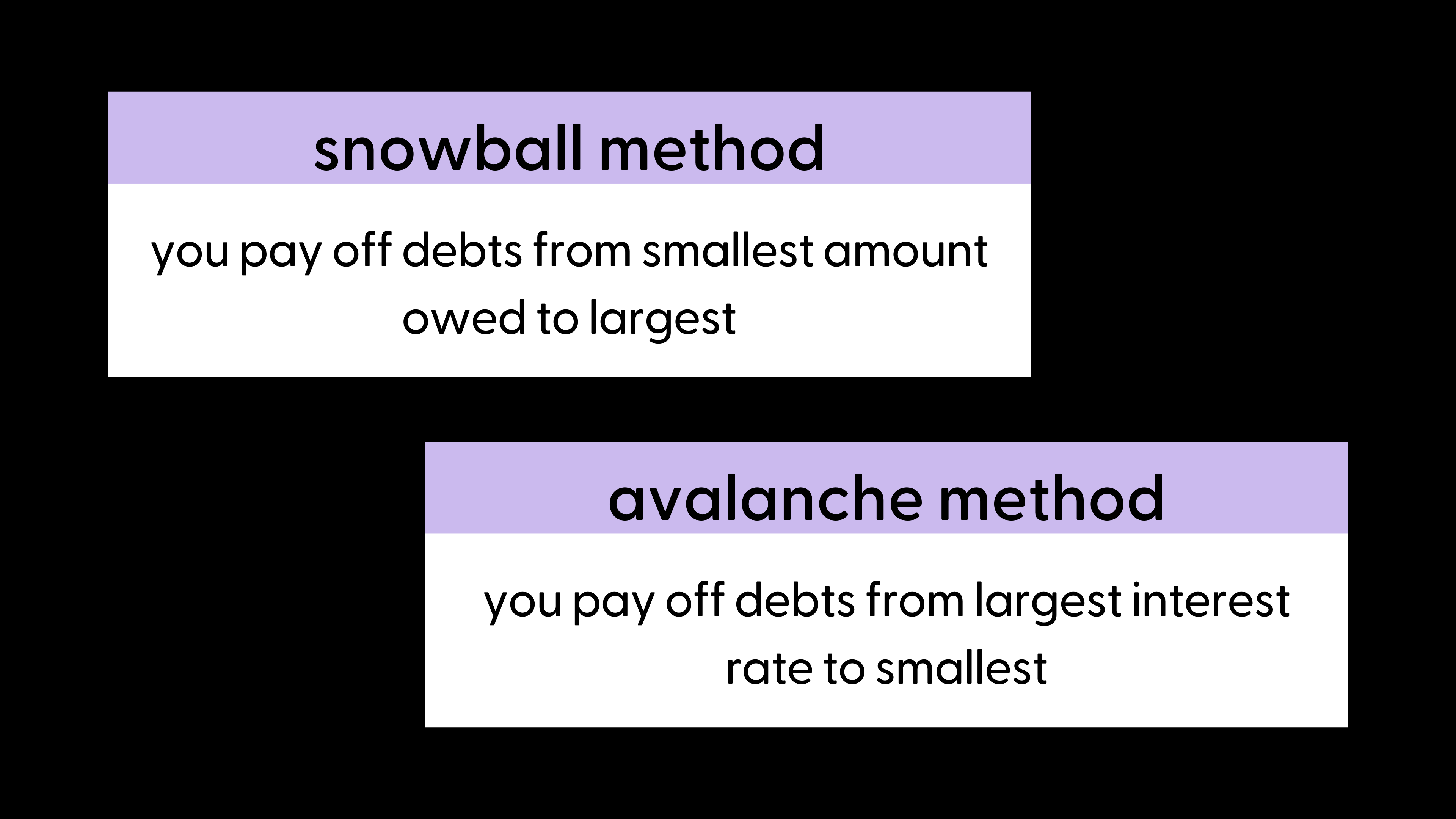

A popular debt strategy is the “avalanche method,” which involves paying off debts starting with the one with the highest interest rate first, then moving on to the next highest interest rate, and so on, saving the most money on interest over time.

Another popular option is the “snowball method,” where you start with the smallest balance first, then moving on to larger balances, regardless of interest rates, to build momentum and motivation.

What we usually recommend to our students is what we call the “intelligent snowball method.” This combines the benefits of the snowball and the avalanche methods.

Essentially, this is when you pay off your smallest debt, then start paying off your debt based on interest rates, going from highest rate to lowest.

Want a boost paying off your debt?

Congratulations! Once you've done all that, you are ready to start paying down your debt.

Speaking of debt, if you want to hear the story of how our Dow Janes co-founder Laurie-Anne paid off $40,000 of debt and built a multi-million dollar investment portfolio, be sure to check out our free masterclass!

A Weekly Sip of Our Best Advice

We respect your privacy. We'll use your info to send only what matters to you — content, products, opportunities. Unsubscribe anytime. See our Privacy Policy for details.